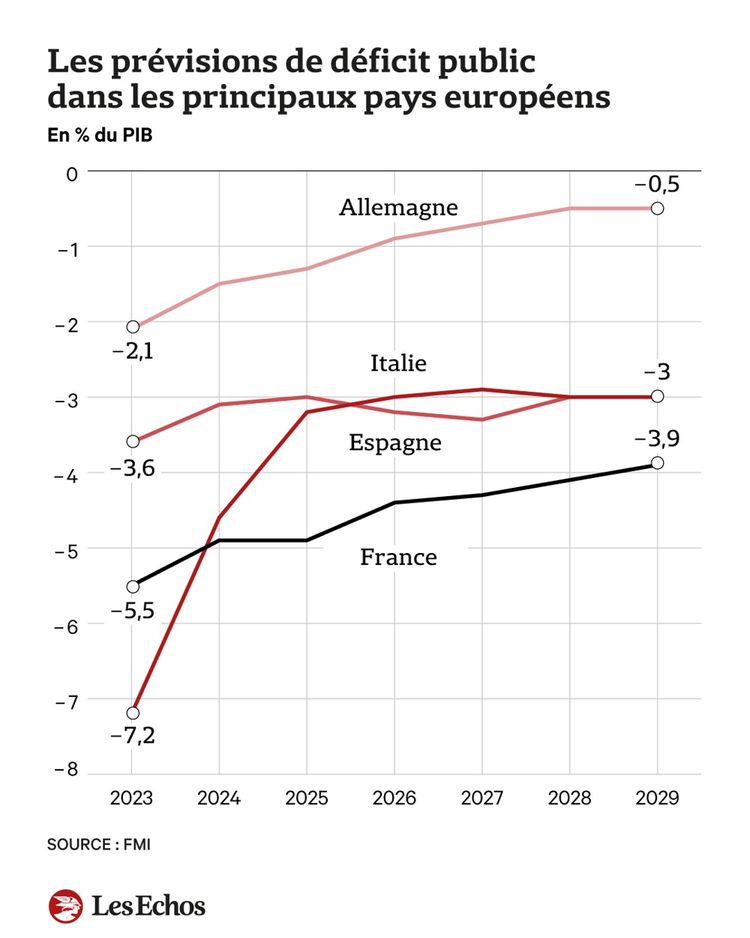

Is the euro zone heading towards new frictions due to the public debt of some of its member states? The question is worth asking when reading the latest economic forecasts from the International Monetary Fund (IMF). These reveal significant future divergences in public debt between the three major economies, Germany, France and Italy.

Despite anemic growth, Germany’s public debt would reduce in the coming years to reach 57.7% of the country’s GDP in 2029, compared to 64.3% at the end of last year. France would see its public debt increase from 107.5% of its GDP to 115.2% in 2029. In five years, the French debt burden would therefore represent double that of Germany, according to the expectations of the international institution in Washington. France would still record a primary public deficit, that is to say before payment of the debt burden, of 1.1% of GDP in 2029. Italy would also show an increase in its public debt in 2029, to 144% of its GDP, an increase of 7 points in five years. The transalpine debt would even be higher than that of Greece at that date.

Worrying divergences

Significant uncertainties obviously weigh on such predictions in a particularly unpredictable world. But the direction is clear with the end of inflation: Germany’s public debt will diverge even more in the coming years from those of its neighbors despite new European budgetary rules. And “this divergence is worrying in a monetary union without a common public treasury and therefore without budgetary transfers to cushion shocks,” considers Pierre Jaillet, researcher at the Institute of International and Strategic Relations (IRIS) and the Jacques Delors Institute.

At a time when we need to invest in technologies, sovereignty and the fight against climate change, the importance of the debt could be a serious handicap. The risk is also political. It is not impossible that a future German government will aggravate tensions by indicting countries which were unable or unable to control their debt.

Pending the emergence of dissensions, the rating agency S&P Ratings must deliver its opinion on the Italian rating this Friday. However, the deterioration of Italian public finances accelerated with Covid, which marked a rupture for the country. Italy had a primary surplus of around 2 points of GDP before the pandemic. It now reaches 3.6%. “So the dynamic is quite worrying. Especially since the debt repayment schedule is important in the short term. Italy should raise 310 billion euros on the markets this year and 340 billion next year,” recognizes an economist from a major French bank.

Investor phlegm

For the moment, the markets remain very calm. “There is no problem with the sustainability of public debt in Europe in the short term because the interest rates, after taking into account inflation, are not that high,” believes Pierre Jaillet.

One of the reasons for investor sluggishness is technical. French public debt securities (OAT) “are the de facto reserve asset for the euro zone since there are simply not enough German Bunds to meet the demand of institutional buyers. Germany invests little, so it borrows little. For 2024, Germany’s issuance program is only 76 billion euros, almost four times less than France which will borrow 285 billion euros,” explains Christopher Dembik, economist at Pictet Asset. Management.

The other explanation is that the European Central Bank (ECB), which is expected to lower its rates in June, has designed an instrument to help countries in difficulty in the summer of 2021, called TPI, which consists of buying public debt. Which reassures investors. But such solutions do not solve long-term structural problems.

Top exit doors could take two forms. First, Germany, which is going through an economic crisis, could end its debt brake which requires its structural deficit not to exceed 0.35% of its GDP. And the country would invest to revive its economy and modernize its industry. This would give some breathing room to the rest of the eurozone. The difficulty with this scenario is that German public opinion is attached to the debt brake.

Then, indebted countries would engage in budgetary efforts. But here again there is an obstacle. It is particularly difficult for a country to reduce the debt burden when growth is weak.